Stocks to Buy Now December 2025")

Best Artificial Intelligence (AI) Stocks to Buy Now December 2025

5 Best AI Stocks to Buy Today

| Company (Ticker) | 12 Week Price Change | Forward PE | Price | Proj EPS Growth (1 Year) | Projected Sales Growth (1Y) |

|---|---|---|---|---|---|

| Micron Technology (MU) | 68.75% | 8.82 | $276.67 | 278.29% | 89.30% |

| Intuitive Surgical (ISRG) | 32.01% | 67.36 | $577.64 | 17.28% | 18.72% |

| NVIDIA (NVDA) | 1.01% | 39.50 | $188.75 | 55.54% | 62.39% |

| Lam Research (LRCX) | 33.69% | 36.59 | $175.52 | 15.70% | 14.11% |

| Teradyne (TER) | 46.82% | 56.21 | $198.85 | 8.97% | 8.06% |

*Updated on December 23, 2025.

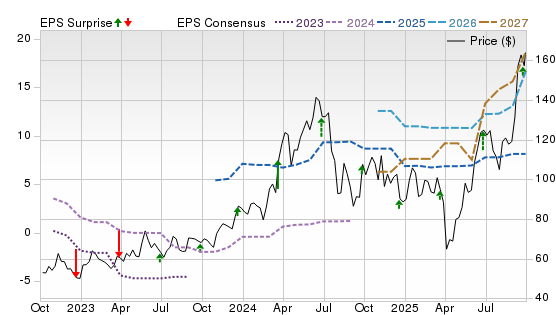

Micron Technology (MU)

$276.67 USD +0.08 (0.03%)

3-Year Stock Price Performance

Premium Research for MU

- Zacks Rank

- Strong Buy 1

- Style Scores

C Value A Growth A Momentum A VGM

- Market Cap: $299.30 B (Large Cap)

- Projected EPS Growth:164.17%

- Last Quarter EPS Growth:61.19%

- Last EPS Surprise:22.25%

- Next EPS Report date:March 19, 2025

Our Take:

Micron is a leading supplier of DRAM, NAND and high-bandwidth memory that sits at the heart of AI accelerators and data-center servers. A Zacks Rank #1 (Strong Buy) reflects brisk upward estimate revisions, while Style Scores of A for Growth and Momentum point to improving earnings power and strong relative strength despite only a mid-pack Value Score of C.

Micron is ramping HBM3E and next-gen DRAM nodes into a tight supply backdrop as hyperscalers build AI clusters. Its HBM3E is qualified for NVIDIA’s H200 platform, positioning Micron to capture multiyear AI infrastructure spending as memory content per GPU surges. Broad AI-driven demand and constrained HBM supply are major tailwinds.

Micron’s Price, Consensus & EPS Surprise chart shows price strength tracking sharply rising 2026–2027 earnings estimates, with a recent pullback met by renewed estimate momentum. Its strategic positioning in the sector makes it a timely AI lever.

See more from Zacks Research for This Ticker

Normally $25 each - click below to receive one report FREE:

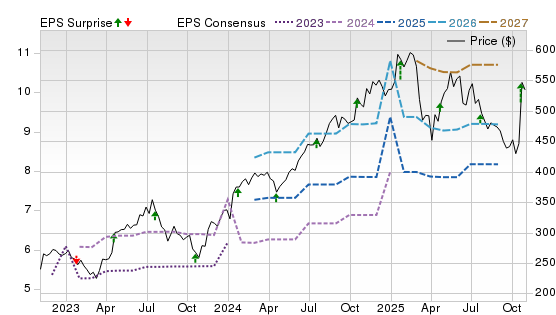

Intuitive Surgical (ISRG)

$577.64 USD -2.19 (-0.38%)

3-Year Stock Price Performance

Premium Research for ISRG

- Zacks Rank

Buy 2

Buy 2

- Style Scores

D Value C Growth F Momentum F VGM

- Market Cap:$205.22 B (Large Cap)

- Projected EPS Growth:17.30%

- Last Quarter EPS Growth: 7.10%

- Last EPS Surprise: 20.60%

- Next EPS Report date: Jan. 22, 2026

Our Take:

Intuitive develops the da Vinci robotic-assisted surgery platform and Ion lung biopsy system, increasingly embedding advanced computing and AI-guided capabilities. A Zacks Rank #1 reflects positive earnings estimate revisions. However, weak Style Scores of F for Value and Momentum and D for Growth show that investors are paying a premium for quality. Near-term share performance has been uneven.

The da Vinci 5 system marks a leap in computing power and real-time data processing. Hospitals are increasingly focused on productivity, efficiency and outcomes. Intuitive’s expanding data, vision, and automation roadmap should raise switching costs, supporting growth.

On the chart, shares have climbed to new highs alongside improving 2026–2027 EPS trajectories after a mid-period dip. New features aim to streamline operating room workflows and deliver insights. These factors will support higher adoption. ISRG offers growth, but procedure volumes and hospital capital spending remain elements to watch.

See more from Zacks Research for This Ticker

Normally $25 each - click below to receive one report FREE:

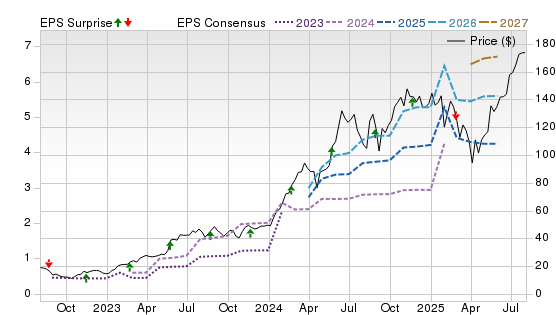

NVIDIA (NVDA)

$188.75 USD +5.06 (2.76%)

3-Year Stock Price Performance

Premium Research for NVDA

- Zacks Rank

Strong Buy 1

Strong Buy 1

- Style Scores

F Value B Growth D Momentum D VGM

- Market Cap: $4,398.06 B (Large Cap)

- Projected EPS Growth: 55.18%

- Last Quarter EPS Growth: 25.25%

- Last EPS Surprise:4.84%

- Next EPS Report date: Feb. 25, 2026

Our Take:

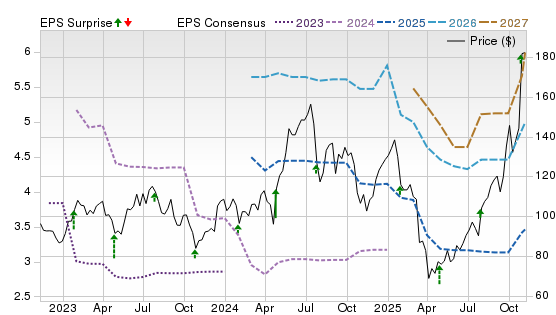

NVIDIA designs the world’s leading AI accelerators, systems, networking and software stack that power training and inference across hyperscale and enterprise workloads. A Zacks Rank #1 reflects persistent positive revisions. Style Scores of F for Value, D for Momentum and B for Growth show premium pricing and intermittent consolidation, amid stable earnings expansion.

The Blackwell platform, spanning B200 and GB200 GPUs, NVLink and software, aims to deliver step-function performance and energy efficiency for trillion-parameter models. These extend NVIDIA’s full-stack moat across silicon, systems and CUDA software. Broad adoption by major clouds and OEMs underscores ecosystem pull-through across data center, networking and platforms.

Its chart features a powerful price advance mirrored by steeply rising 2026–2027 EPS consensus lines. Occasional price volatility hasn’t derailed upward revisions, which supports a constructive view. For AI exposure, NVDA remains a core holding, backed by strong ecosystem lock-in and rapid product cycles.

See more from Zacks Research for This Ticker

Normally $25 each - click below to receive one report FREE:

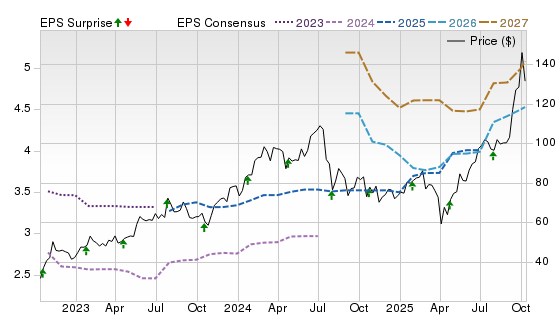

Lam Research (LRCX)

$175.52 USD +0.26 (0.15%)

3-Year Stock Price Performance

Premium Research for LRCX

- Zacks Rank

- Buy 2

- Style Scores

D Value A Growth C Momentum B VGM

- Market Cap:$216.38 B (Large Cap)

- Projected EPS Growth:15.70%

- Last Quarter EPS Growth:-5.26%

- Last EPS Surprise:4.13%

- Next EPS Report date:Feb. 4, 2026

Our Take:

Lam Research supplies critical etch and deposition tools used to manufacture leading-edge logic, 3D NAND and high-bandwidth memory, key building blocks for AI compute. A Zacks Rank #2 (Buy) indicates favorable, though moderating, estimate revision trends. Style Scores of D for Value, A for Growth and C for Momentum reflect a strong earnings trajectory, despite less appeal on valuation.

AI’s memory intensity and HBM stacking are driving demand for wafer-fab-equipment, where Lam’s process tools and packaging know-how are essential. Updates from the company and industry reports highlight rising AI-related orders, with Lam introducing new deposition capabilities while calling out demand tied to HBM and advanced nodes.

The chart shows a steady uptrend as 2025–2027 EPS estimates grind higher, validating its growth path. While momentum is cooler than earlier in the cycle, the alignment of improving consensus and price supports a constructive intermediate outlook.

See more from Zacks Research for This Ticker

Normally $25 each - click below to receive one report FREE:

Teradyne (TER)

$198.85 USD +1.63 (0.83%)

3-Year Stock Price Performance

Premium Research for TER

- Zacks Rank

- Buy 2

- Style Scores

D Value F Growth D Momentum F VGM

- Market Cap:$30.57 B (Large Cap)

- Projected EPS Growth:9.01%

- Last Quarter EPS Growth:49.12%

- Last EPS Surprise: 8.97%

- Next EPS Report date: Feb. 4, 2026

Our Take:

Teradyne is a leading provider of semiconductor test equipment and industrial automation, built around collaborative robots. A Zacks Rank #2 signals favorable estimate revisions. Style Scores of D for Value and Momentum and F for Growth indicate valuation and earnings-quality headwinds, typical early in cyclical recoveries.

AI accelerators, HBM and advanced packaging are driving more complex test requirements, benefiting Teradyne’s memory and compute test franchises. Management recently cited AI-related demand as a key tailwind in results, with memory test notably strong, while longer-term robotics adds optionality as factories adopt automation. It will gain from high-parallel, high-speed test intensity, while cycle timing keeps results sensitive to ordering patterns.

On the chart, TER’s price has been volatile but is rebounding as 2026–2027 EPS estimates turn up from trough levels. That improving revision trend suggests the stock could have leverage to a sustained AI-hardware test cycle, despite an uneven momentum.

See more from Zacks Research for This Ticker

Normally $25 each - click below to receive one report FREE:

Methodology

The Zacks Rank is a proprietary stock-rating model that uses trends in earnings estimate revisions and earnings-per-share (EPS) surprises to classify stocks into five groups: #1 (Strong Buy), #2 (Buy), #3 (Hold), #4 (Sell) and #5 (Strong Sell). The Zacks Rank is calculated through four primary factors related to earnings estimates: analysts' consensus on earnings estimate revisions, the magnitude of revision change, the upside potential and estimate surprise (or the degree in which earnings per share deviated from the previous quarter).

Zacks builds the data from 3,000 analysts at over 150 different brokerage firms. The average yearly gain for Zacks Rank #1 (Strong Buy) stocks is +23.62% per year from January, 1988, through June 2, 2025.

Selections for Best AI Stocks are based on the current top ranking stocks based on Zacks Indicator Score. For this list, only companies that have average daily trading volumes of 100,000 shares or more and at least five analysts covering the stock were considered. All information is current as of market open, Dec. 22, 2025.

Guide to AI Stocks

The classification of “AI Stocks” is actually quite broad, ranging from companies that provide the essential hardware, companies that create the software to run Large Language Models, and a whole host of other industries and companies that are creating the Artificial Intelligence ecosystem. All stand to gain – or lose – depending on the fortunes of AI tech.

Types of AI Stocks

Hardware (GPUs, Chips) Stocks – NVIDIA, AMD, TSMC, Broadcom

The backbone of AI is raw computing power, and this comes primarily from specialized chips like graphics processing units (GPUs) and AI-focused accelerators. NVIDIA (NVDA) is the undisputed leader in GPUs used for training large language models.

Advanced Micro Devices (AMD) is a rising competitor, with its MI300 series targeting data center AI workloads. Taiwan Semiconductor Manufacturing Co. (TSMC) doesn’t make its own chips but manufactures advanced nodes for nearly every big tech firm—including Apple, Nvidia, and AMD—making it critical to the global AI supply chain. Broadcom (AVGO) has carved a niche in custom ASICs (application-specific integrated circuits) for hyperscale cloud providers, which value tailored chips that reduce energy use and maximize throughput.

These companies benefit from structural demand for more computing capacity, but they also face geopolitical risks such as U.S.-China export restrictions and cyclical swings in semiconductor demand.

AI Cloud & Infrastructure – Microsoft, Amazon, Alphabet

Building AI applications at scale requires massive computing infrastructure. Azure from Microsoft (MSFT) has become a leader by integrating OpenAI’s models directly into its cloud offerings, giving it a first-mover advantage in AI enterprise adoption. Amazon Web Services, a subsidiary of Amazon (AMZN) is deploying its in-house Trainium and Inferentia chips, aiming to lower costs for AI workloads while retaining dominance in cloud services. Alphabet’s (GOOG) Google Cloud is leaning heavily on its proprietary Tensor Processing Units (TPUs) and Gemini AI models to differentiate itself.

Investing in these players is less about speculative growth and more about diversified tech giants whose AI investments bolster an already profitable core business.

Enterprise AI Software & Analytics – Palantir, C3.ai, Adobe, Snowflake

AI isn’t just about hardware; software platforms are where businesses actually apply machine intelligence. Palantir (PLTR) powers decision-making for defense and large corporations with its Foundry and Gotham platforms. C3.ai (AI) focuses specifically on AI-driven applications across industries like energy, finance, and manufacturing. Adobe (ADBE) has integrated AI across its creative suite (e.g., Firefly in Photoshop), while Snowflake (SNOW) has added AI-enabled analytics to its cloud data warehousing business.

These stocks tend to have higher growth potential but also higher risk, as adoption timelines and customer budgets can vary widely.

Cybersecurity AI – CrowdStrike

The rise of AI also heightens cyber risks. CrowdStrike (CRWD) leads in AI-powered threat detection, using machine learning to flag suspicious behavior across millions of endpoints in real time. With ransomware and nation-state attacks increasing, demand for AI-driven security remains strong. Cybersecurity names often benefit from recurring revenue models, which may help smooth out volatility compared to hardware peers.

Benefits and Risks of AI Stocks

Benefits:

- Secular Growth: AI adoption is still in early innings, with enterprise use cases expanding rapidly.

- Diversified Exposure: Investors can target infrastructure, software, or services depending on risk tolerance.

- First-Mover Advantage: Leaders like NVIDIA and Microsoft are shaping the ecosystem, creating strong economic moats.

Risks:

- Valuations: Many AI leaders are priced for perfection, leaving little margin of safety.

- Hype Cycle: Investor enthusiasm may outrun near-term fundamentals, creating bubble risk.

- Regulation: Governments are exploring AI rules around privacy, bias, and national security, which could reshape business models.

- Competition: Barriers to entry are high, but fast innovation means today’s leader can quickly lose ground.

How to Choose AI Stocks

When evaluating AI stocks, consider:

- Revenue Mix: How much of the company’s growth is truly driven by AI vs. traditional segments?

- Moat & Differentiation: Does the company control unique technology (like NVIDIA’s CUDA software ecosystem)?

- Customer Adoption: Look for companies with recurring contracts or wide adoption across industries.

- Financial Health: Strong balance sheets matter in a capital-intensive industry.

- Valuation Metrics: Compare price-to-earnings (P/E) ratio, price-to-sales (P/S) ratio, and forward growth projections to industry peers.

How to Invest in AI Stocks

There are multiple entry points depending on your goals:

- Direct Stock Picks: Best if you want concentrated exposure to specific company leaders or disruptors.

- AI Exchange-Traded Funds (ETFs): ETFs such as Global X Robotics & Artificial Intelligence ETF (BOTZ) or iShares Robotics and AI ETF (IRBO) provide diversification by investing in a broad range of companies in the AI space.

- Broad Tech ETFs: Like Invesco QQQ (QQQ) or Vanguard Information Technology ETF (VGT), offering AI exposure as part of a bigger tech basket.

- Dollar-Cost Averaging (DCA): A strategy to smooth price volatility by buying at regular intervals AI stocks or funds.

- Long-Term Holds: Since AI is a multi-decade trend, investors who can weather short-term swings may see the best results.

AI Stocks Alternatives

If you want exposure to AI without betting on a single stock:

- ETFs: Offer diversification and reduce single-company risk.

- Private Markets: Startups in robotics, generative AI, and enterprise AI could offer upside, though access is limited to accredited investors, which face income or licensing limitations (such as a net worth of $1 million, excluding primary residence, plus a high annual income – $300,000 if married.

- Picks-and-Shovels Plays: Companies supplying infrastructure, like power management (e.g., Eaton) or data center REITs (e.g., Equinix), benefit indirectly from AI growth.

Strategies for AI Stocks Moving Forward

- Barbell Approach: Combine stable mega-caps (Microsoft, Nvidia) with speculative names (Quantum Computing Inc., Credo) for balanced exposure.

- Rebalancing: Trim positions after strong rallies to lock in gains and redeploy into underweighted sectors.

- Monitor Earnings: Focus on whether AI adoption translates into sustainable revenue growth.

- Look Beyond the U.S.: Consider emerging AI leaders in Europe and Asia for diversification.

- Stay Agile: AI is evolving rapidly; reassess holdings every quarter as new winners emerge.

Frequently Asked Questions About AI Stocks

Are AI stocks overvalued?

Many AI leaders are priced at steep multiples compared to the broader market. That doesn’t mean all are bubbles, but investors should separate hype from earnings-driven growth.

What is the forecast for AI stocks?

Most analysts expect AI demand to expand through at least the next decade, with data center spending, AI-as-a-service, and AI-enabled enterprise tools driving revenue.

What metrics best signal AI efficacy?

- Growth in AI-specific revenue lines.

- Gross margin improvements tied to AI.

- Customer retention and expansion.

- Evidence of scale: Contracts, partnerships, recurring revenue.